Weekly Economic Update

Presented by Bolls and Wells Wealth Management August 12, 2024

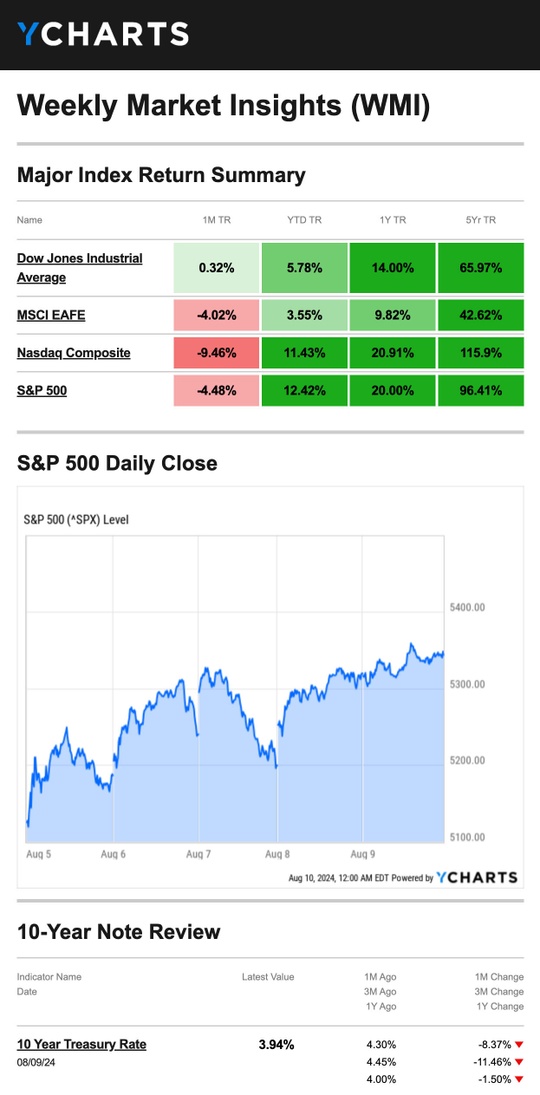

| Stocks ended last week with modest losses, masking a volatile five-day trading period that saw investors embrace recession concerns and then dismiss the slow-down talk as speculation as the week progressed.

The Dow Jones Industrial Average slipped 0.60 percent, while the Standard & Poor’s 500 Index ended flat (-0.04 percent). The Nasdaq Composite dipped 0.18 percent. The MSCI EAFE Index, which tracks developed overseas stock markets, fell 1.21 percent.1,2 Stocks Stage ComebackMonday was the worst day for the S&P 500 and the Dow in nearly two years. As recession talk grew louder, investors took a “risk off” position. On Monday, the Japanese market had its worst drop since 1987 as market participants unwound positions from a popular trading strategy called a “carry trade” amid a global sell-off in stock prices.3 But on Thursday, initial jobless claims fell less than expected—a positive sign for the labor markets— which quieted some of the recession talk. Also, as the week progressed, there was growing speculation that the July jobs report was more of an outlier than a lead indicator of a pending recession. By Friday’s close, all three major averages had regained most of the week’s losses.4 |

|

|

|

|

Mortgage UpdateLast Thursday, the average rate on a 30-year fixed mortgage dropped to 6.47 percent—a 15-month low. Many home buyers welcomed the news, and it appeared to help support Thursday’s rally.5 But the announcement left some wondering whether rates would continue to trend lower. Mortgage rates are tied to the interest rates set by the Federal Reserve. Some speculated the drop was due to market participants anticipating the Fed would adjust rates in September, which remains anything but certain.6 This Week: Key Economic DataTuesday: Producer Price Index (PPI). Fed Official Raphael Bostic speaks. Wednesday: Consumer Price Index (CPI). EIA Petroleum Status Report. Thursday: Jobless Claims. Retail Sales. Industrial Production. Business Inventories. Fed Officials Alberto Musalem and Patrick Harker speak. Friday: Housing Starts and Permits. Consumer Sentiment. Fed Official Austan Goolsbee speaks. Source: Investors Business Daily – Econoday economic calendar; August 8, 2024 This Week: Companies Reporting EarningsTuesday: The Home Depot, Inc. (HD) Wednesday: Cisco Systems, Inc. (CSCO) Thursday: Walmart Inc. (WMT), Applied Materials, Inc. (AMAT), Deere & Company (DE) Source: Zacks, August 8, 2024 |

|

| “When things go wrong, you’ll find they usually go on getting worse for some time; but when things once start going right they often go on getting better.”

– C.S. Lewis |

|

Divorce or Separation Can Affect Your TaxesThe first thing to consider is alimony payments. Alimony payments paid under a divorce or separation instrument are deductible by the payer, and the recipient must include it in income. Alimony is not subject to tax withholding, so increasing the tax paid during the year may be necessary to avoid a penalty. The next thing to consider is IRA contributions. A divorce agreement by the end of the tax year means taxpayers can’t deduct contributions made to a former spouse’s traditional IRA. They can only deduct contributions made to their own traditional IRA. Once you reach age 73, you must begin taking RMDs from a traditional IRA in most circumstances. Withdrawals from traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. *This information is not intended to be a substitute for specific, individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax professional. Tip adapted from IRS.gov7 |

|

3 Yoga Poses for BeginnersThe first pose is a downward-facing dog used in most yoga practices. In it, you have your arms stacked under your shoulders, your bottom in the air, and your back legs straight. Your body is in the shape of an upside-down “V.” The next is Crescent Lunge. Stand in a forward lunge with one foot in front and bent. Your back leg is straight. Now, straighten your arms and lift them over your head. This pose is often used in yoga flow classes. Last, we have the Triangle pose. Step your feet apart (wider than your shoulders). Then, hinge at your hip and lean over your front leg. Reach down with the same arm in front and rest it on the floor or a yoga block. Tip adapted from SELF Magazine8 |

|

| There are three cups of flour on a counter and you take one away. How many cups of flour do you have now?

Last week’s riddle: A cat falls into a hole 14.5 feet deep. The cat can jump 3 feet high, but she slides back 1 foot with each jump. How many jumps does it take her to get out of the hole? Answer: Every 3-foot jump accompanied by a 1-foot slide equals jumps of 2 feet high each; at that rate, the cat’s seventh jump, starting at 12 feet, will leave her 15 feet above the bottom of the hole so that she may escape. |

|

|

| Hirosaki castle, Hirosaki, Japan |

Footnotes and Sources1. The Wall Street Journal, August 9, 2024 2. Investing.com, August 9, 2024 3. CNBC.com, August 5, 2024 4. The Wall Street Journal, August 8, 2024 5. The Wall Street Journal, August 8, 2024 6. The Wall Street Journal, August 9, 2024 7. IRS.gov, May 8. 2024 8. SELF Magazine, May 8, 2024 |